Most WorkTech businesses had a difficult trading in the last 18 months, with business spending and hiring remaining subdued across Europe and North America. Still, the first two quarters of the year show a booming M&A market and gradual recovery in VC sentiment. We expect the latter to accelerate in the coming quarters, especially for later-stage financings as investors resume their support for the new wave of leaders in the space. Every quarter seems to be better than the previous one, and Q4 could be the strongest we will have seen in two years.

The first quarter of 2024 kicked off with a 30% quarterly increase in VC funding, but deal volume remained flat. Revenue growth for most businesses slowed materially in 2023. So what are the most recent expectations for the coming quarters? In this report we explore what the Q1 numbers mean for the sector, what is the outlook for 2024 and 2025, how has M&A activity been developing, and what are latest valuation multiples and trends.

As 2024 gets underway, companies and investors across all sectors look forward to a respite from the difficult narrative of 2023. In this report, we look at what happened in HR Tech and Work Tech during the last 12 months, including: historical and projected company growth rates, investment activity breakdown, M&A activity, trading and transaction valuation multiples, notable transactions.

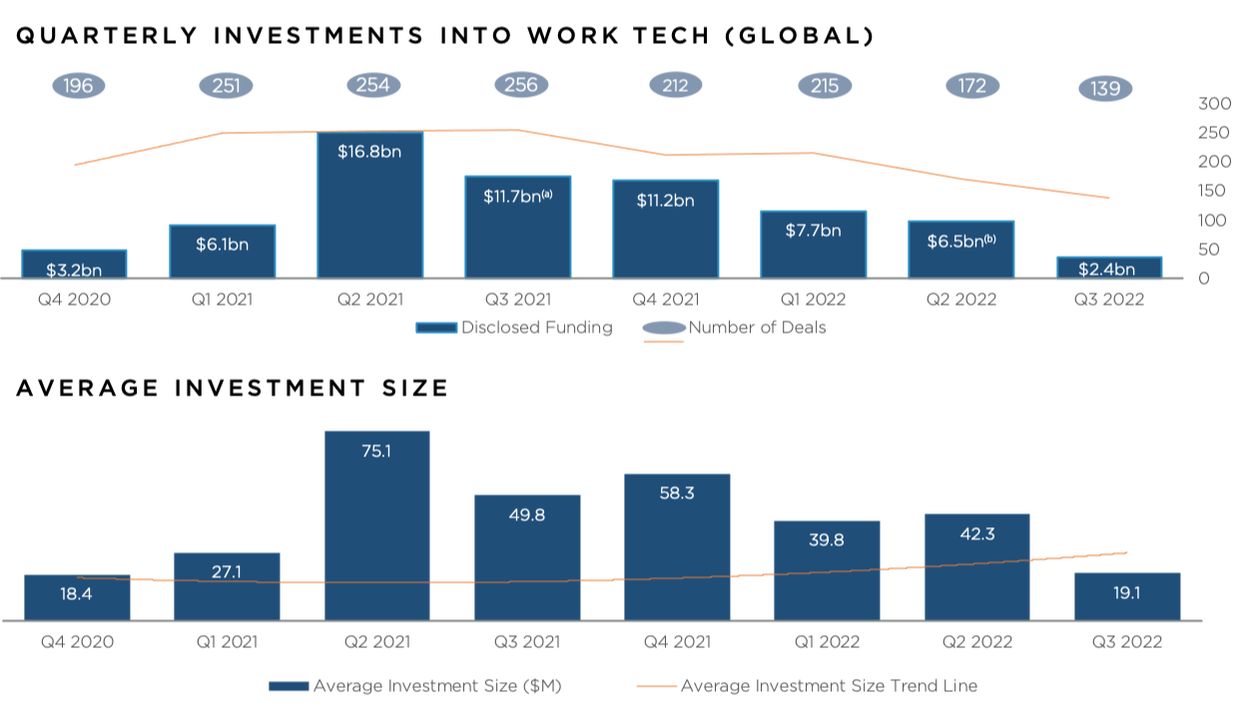

M&A activity held up surprising well during the first half of 2023, with 155 announced acquisitions. This is not far off the robust levels seen in the dealmaking boom of the 2021-2022 post-Covid era. Buyers have remained active, and valuations have shown signs of recovery after contracting by c. 35% last year.

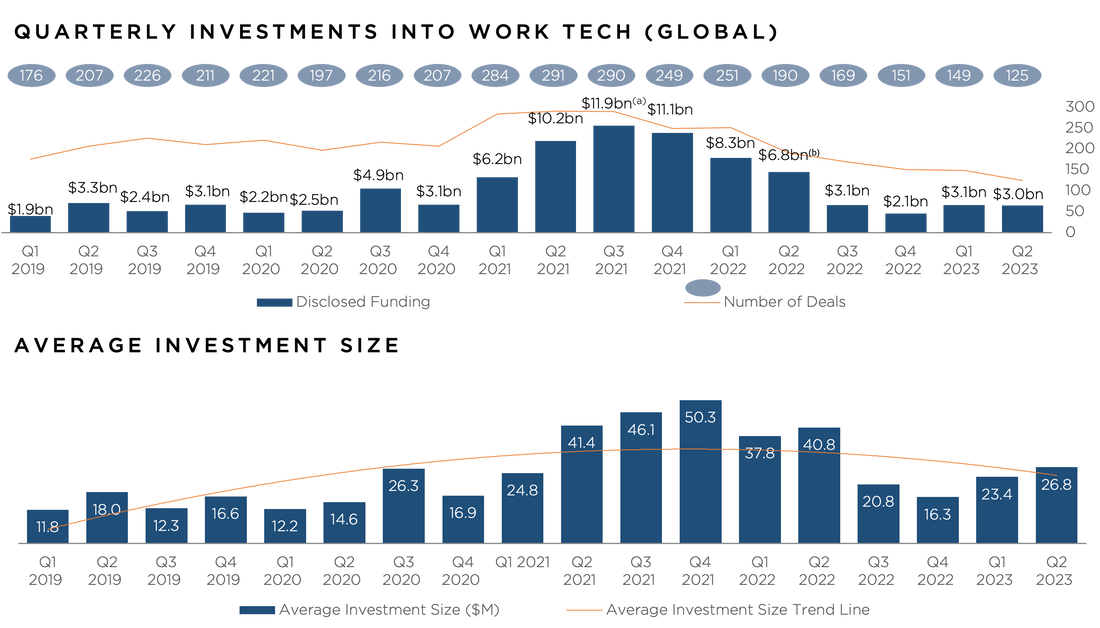

Growth remains the primary valuation driver for M&A. However, increasingly it is assessed in conjunction with capital efficiency, profitability, or with the potential for a business to achieve breakeven in the near term. Equity funding reached $6.1 billion in the first six months of the year, putting 2023 on track to be the third best year in terms of funding for the sector. However, this amount was invested across 274 transactions, which is a record low number of deals for the sector.  Work Tech vendors have been investing in AI for years, yet generative AI will disrupt the Future of Work more quickly than people anticipate, and the impact will be much more pronounced.

In this report we discuss why and how Generative AI will fundamentally change the competitive landscape, and why Work Tech vendors will need to establish a different competitive moat. We dive into the state of the Work Tech market, Generative AI use cases, early product releases, risks, limitations, as well as implications for M&A and VC funding. The report also looks at the impact of inflation, layoffs, lack of VC funding and tightening budgets on Work Tech vendors, and the outlook for M&A and fundraising. Current risks and limitations notwithstanding, the AI genie is now out of the bottle. As with other paradigm-shifting innovations, like the rapid democratization of the Internet following the release of the first Mosaic web browser, all vendors should take note and carefully assess the impact Generative AI is likely to have on their business.  It may not feel this way, but Work Tech is gearing up for a robust M&A recovery in 2023. Following a pause in new process launches last year, there is a notable uptick in businesses looking to explore strategic options this year. For some this is a necessity, with venture funding less abundant and some customers, particularly in tech, tightening their purses. For others, KPI’s have remained robust, and coming to market is a choice contingent only on sentiment improving – or at least stabilizing.

In terms of numbers, 47 Work Tech acquisitions were announced in Q1 2023. This is a c. 45% drop compared to the 84 per quarter, on average, announced during the previous four quarters. Considering the c. 6-9 month lag between an M&A process launching and it being announced, today’s numbers reflect last year’s slowdown.  Companies interested in tapping the debt financing market should note that lenders today are equipped with all-weather intelligence and decision-making frameworks. This facilitates continuity of lending activity during periods of high or low inflation and interest rates, positive or negative economic outlook, financial and geopolitical disruptions, and the likelihood of corporates' distress. As such, 2023 is unlikely to mark a departure from the lenders’ strategies and tactics of 2022. Instead, we are seeng creative approaches to debt financing structures, increased enthusiasm for quality deals and a greater focus on earlier start to relationship-building with borrowers.

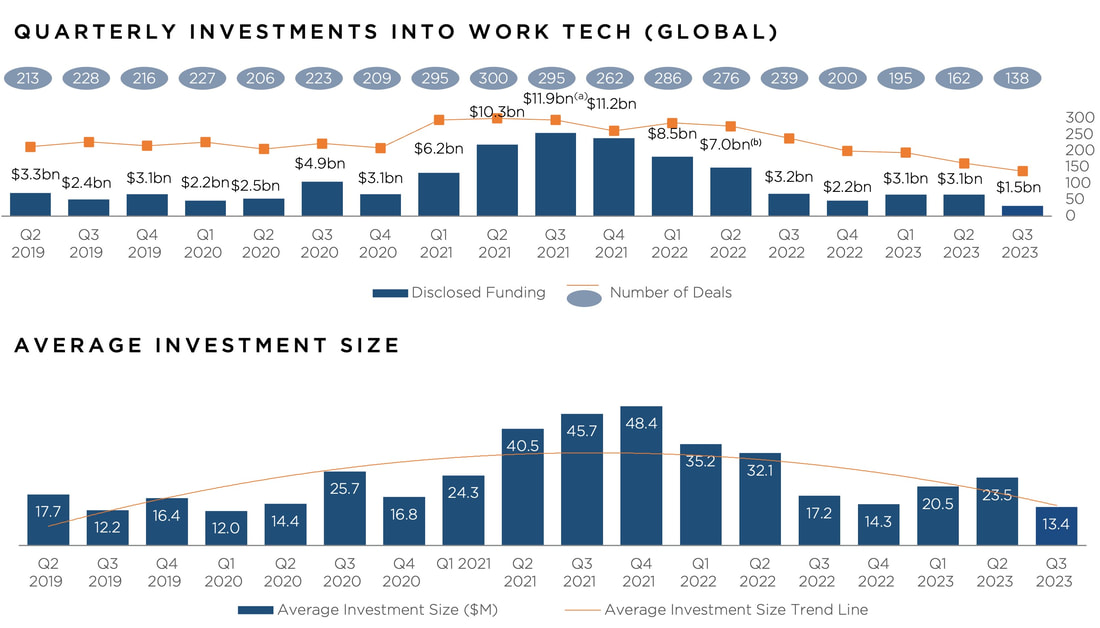

The macro narrative in 2022 was dominated by high inflation, the possibility of an economic recession, and disrupted asset values, particularly high-valued technology stocks. For HR Tech and Work Tech businesses, this narrative had the most profound impact on capital raising, which saw volumes drop to $2.0bn in Q4, levels last seen in Q2 2020, at the peak of the Covid-19 pandemic. However, total funding in 2022 was $19.4bn – a record amount, eclipsed only by the $46.1bn raised in 2021 and higher than the $12.7bn raised in 2020. M&A volumes remained resilient for most of the year, with the effects of the adverse market sentiment not appearing until Q4, reflecting the slowdown in new deal originations earlier in the year.

As we move into 2023, we expect that these themes will continue to affect sentiment in HR Tech and Work Tech. However, their impact will likely change due to the swift tightening of monetary policy in the US and Europe, which has started to affect a range of areas in the economy and capital markets, including inflation, consumption, employment, and business investment. If inflation in the US and Europe continues to decline without a sharp increase in unemployment, this would imply a higher probability of a much-desired soft landing–a scenario that many thought very unlikely just a few months ago.  Following a very strong recovery in 2021 and an initial softening in 1H 2022, the HR Tech and broader Work Tech businesses are adjusting to a new normal. This involves lower growth expectations for 2023 and emphasis on cashflow & profitability. In this context, Q3 shaped up as follows:

|

RSS Feed

RSS Feed

|

Venero Capital Advisors offers tailored and independent investment banking services to businesses operating in HR Tech and the Future of Work sector. Our client relationships are built and carefully maintained on trust, discretion and dedication. We combine in-depth industry expertise with market leading advisory skills – delivered within a highly confidential and unconflicted framework.

Venero Capital Advisors Ltd. is authorised and regulated by the Financial Conduct Authority (the "FCA"), appearing on the FCA register under firm reference number 795179. © Copyright 2023 Venero Capital Advisors Ltd. |