Following a very strong recovery in 2021 and an initial softening in 1H 2022, the HR Tech and broader Work Tech businesses are adjusting to a new normal. This involves lower growth expectations for 2023 and emphasis on cashflow & profitability. In this context, Q3 shaped up as follows:

- M&A activity began to soften, reflecting the abrupt divergence of valuation expectations that occurred in H1. However, acquirers remain active and sellers coming to market can expect to receive a greater share of the buyers’ attention

- Valuations contracted at the top end, but remained unchanged for businesses already valued less aggressively

- Venture investment saw a significant pullback, particularly for later-stage transactions; Investors are taking a more cautious view when assessing opportunities; valuations are coming off of the most excessive levels and rounds take longer to close

Both in M&A and venture, there are two types of buyers / investors: those who take a “risk-off” approach across the board, and those who are more nuanced when assessing opportunities. Valuation expectations between companies and buyers / investors diverged somewhat abruptly in Q2, particularly for businesses that have yet to feel any adverse impact to their operations. However, we are still at the beginning of what is likely to be a protracted battle against recessionary forces. We expect that the current sentiment dichotomy will become more evident during Q4 and Q1 2023, in the form of lower activity, before the level of impact on businesses gradually becomes clearer and viewpoints start to reconverge.

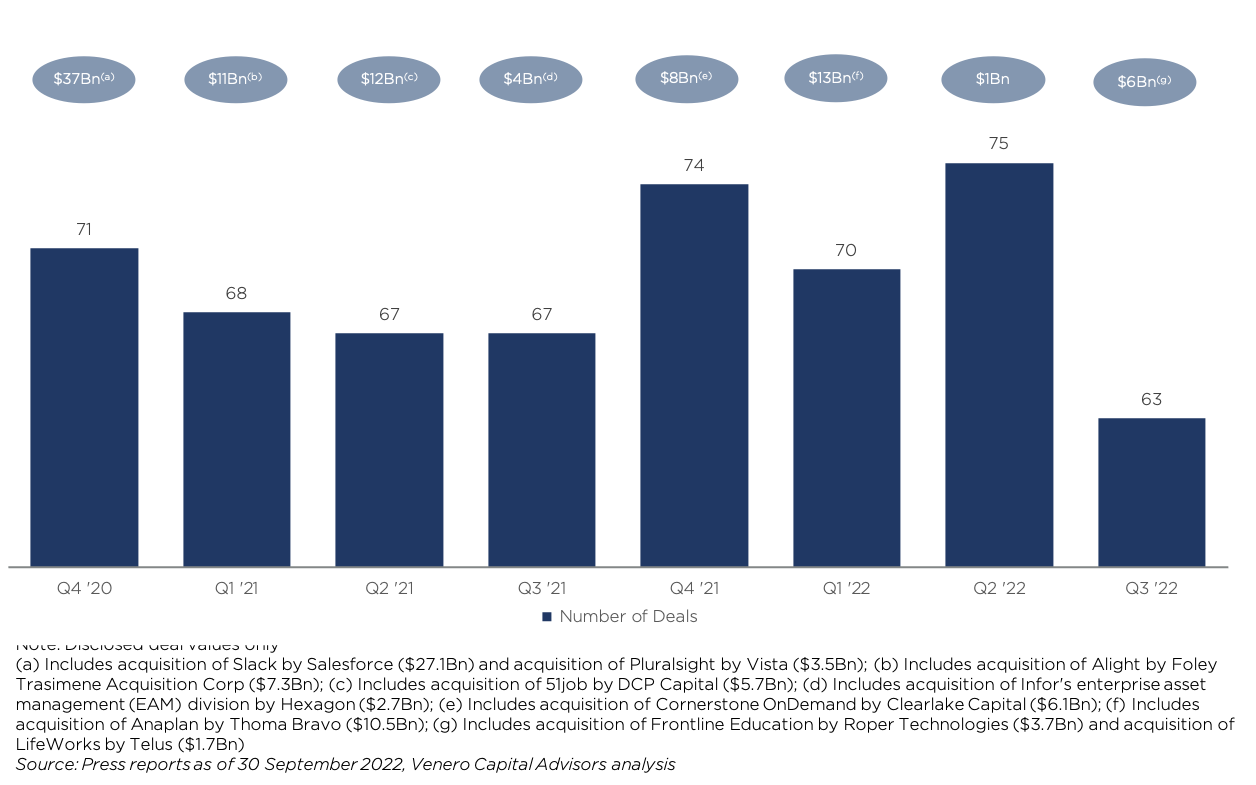

Work Tech M&A Volume and Value

In Q1, valuation expectations between buyers and sellers diverged somewhat abruptly, particularly for businesses that had yet to feel an impact from macro headwinds. Considering there is a 6-9 month lag between an M&A process kicking off and being publicly announced, the first signs of this softening only appeared in Q3 and are likely to trickle into 2023.

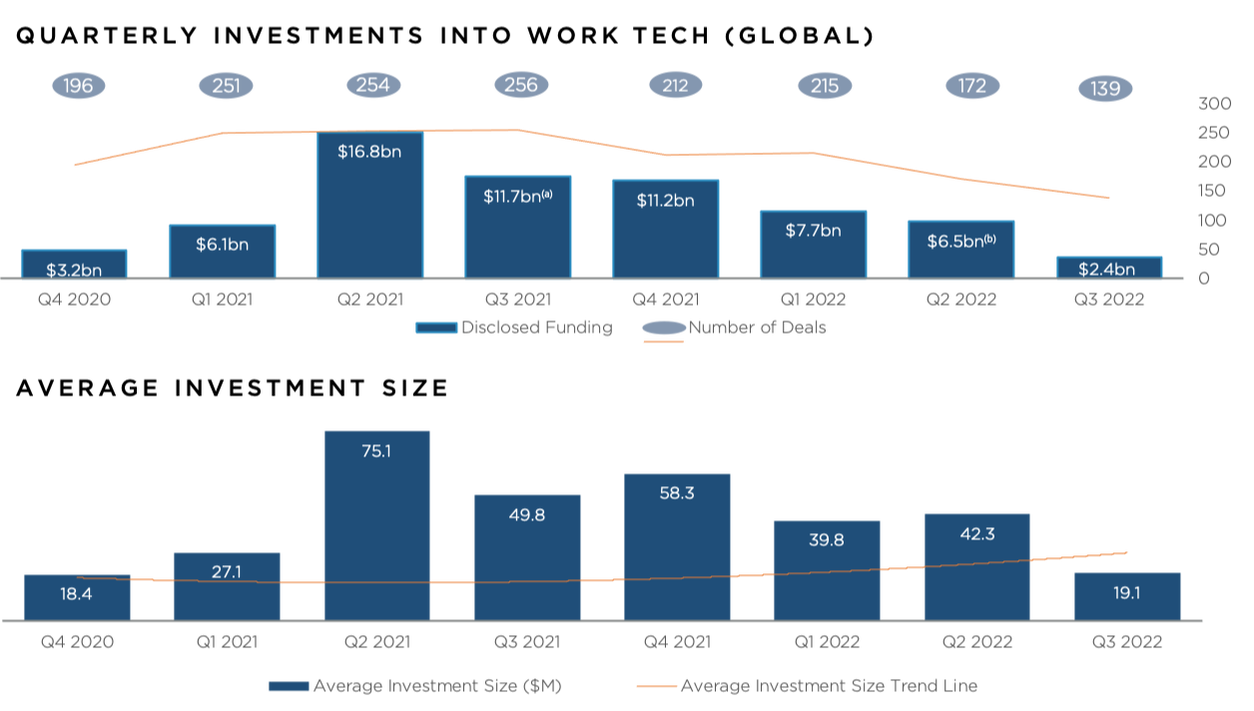

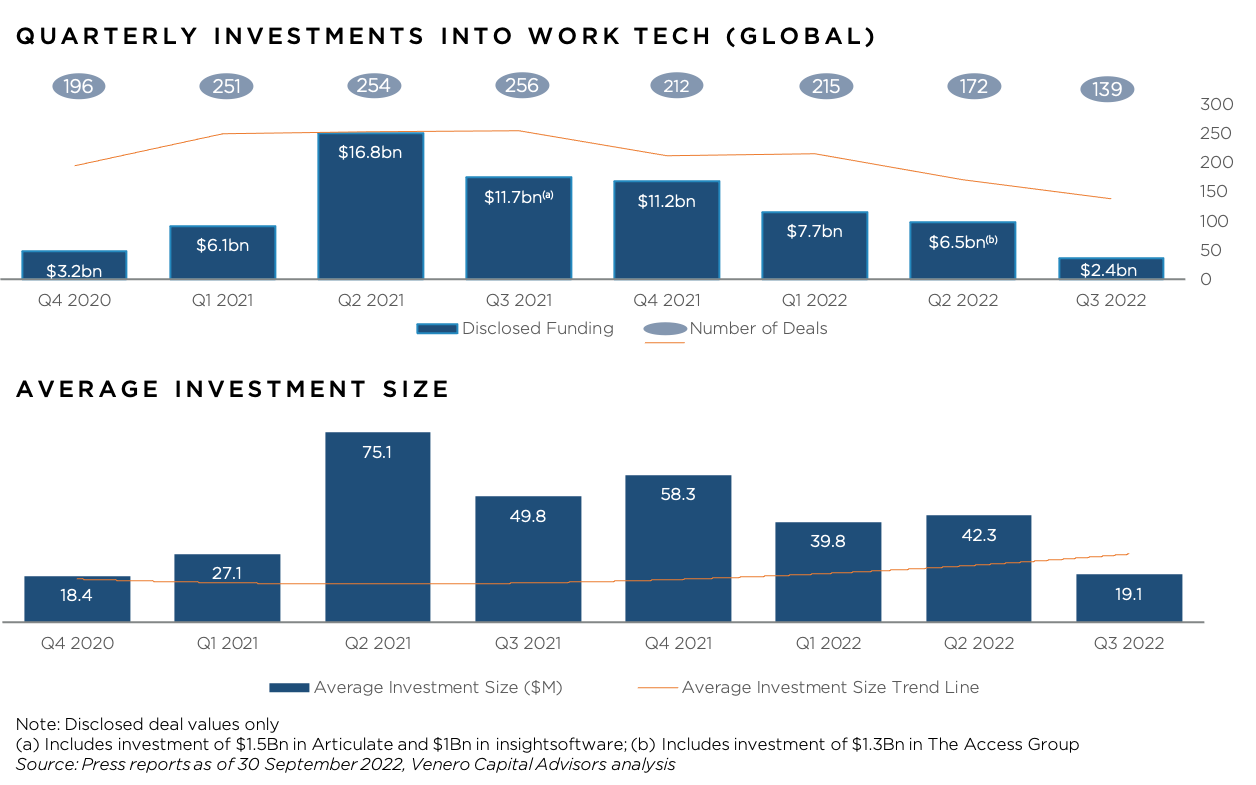

Investment Activity

A total of $2.4Bn was invested in the sector during Q3 2022 across 139 deals. The slower capital deployment is due to increased selectivity on behalf of investors assessing opportunities, longer diligence processes and less urgency.Average investment size contracted to $19.1M vs. $42.3M in the previous quarter. This is well off the peaks of 2021, which had several deals in excess of $100M, and in line with Q4 2020.

.webp)