Following a very strong recovery in 2021 and an initial softening in 1Q 2022, the HR Tech and broader Work Tech sectors are beginning to feel the impact of high inflation and uncertain macroeconomic outlook. In this context, the second quarter closed with mixed results:

- M&A activity held up; Valuations contracted on the high end, but remained unchanged for businesses already valued more modestly; Buyers remain active and corporates exhibit greater conviction in the face of uncertainty than financial acquirers

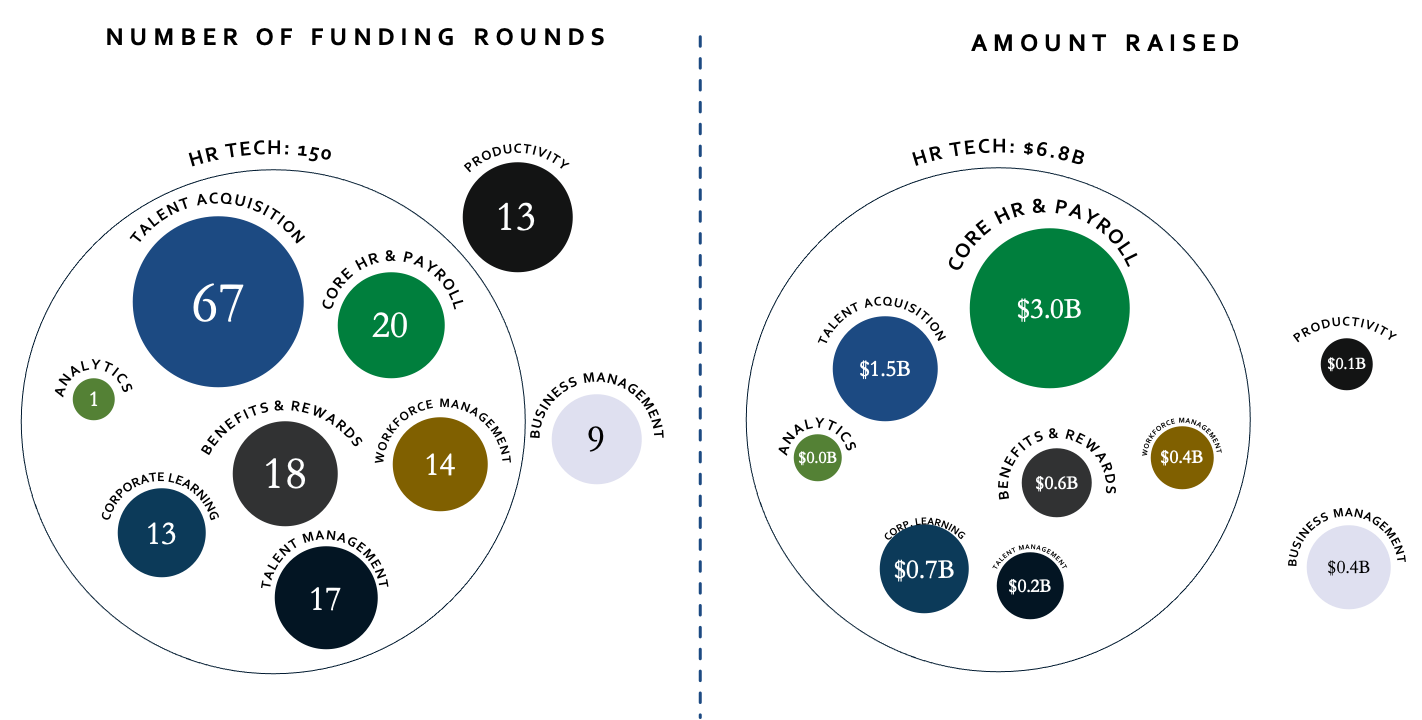

- Venture investment saw a significant pullback, particularly for later-stage transactions; Investors are taking a more cautious view when assessing opportunities; valuations are coming off of the most excessive levels and rounds take longer to close

Both in M&A and venture, there are two types of buyers / investors: those who take a “risk-off” approach across the board, and those who are more nuanced when assessing opportunities. Valuation expectations between companies and buyers / investors diverged somewhat abruptly, particularly for businesses that have yet to feel any adverse impact to their operations. However, we are still at the beginning of what is likely to be a protracted battle against recessionary forces.

We expect that the current sentiment dichotomy will be reflected more comprehensively in the figures of Q3 and Q4, before the level of impact on businesses gradually becomes clearer and viewpoints start to reconverge.

.webp)